What on Terra (Luna) is happening with UST!?

What on Terra (Luna) is happening with UST!?

In case you just woke up from an extended party binge last weekend, here’s the major news of the week: UST has broken its peg, LUNA’s price tanked by a jaw dropping 97.5% in a week (at the time of writing) and the overall crypto market is bleeding red everywhere.

On Saturday May 7th, UST lost its peg to the US Dollar for the first time, hovering at around $0.98. Slightly worrying, however minor depegging events happen with algorithmic stablecoins somewhat often and the forces of supply and demand + a touch of greed usually bring the price back to equilibrium. This wasn’t the case this time. On May 9th, the peg completely went out of control and dropped UST down to $0.76. Some hope was regained the next day as the LFG (Luna Foundation Guard) dipped into its $1B+ BTC reserve to stabilize the peg, making it hover between roughly $0.90-0.93. On May 11th the peg completely tanked, reaching as low as $0.26 at the time of this writing, timestamped on the chart below.

This is arguably the most consequential event in crypto this year so far and while there are many moving parts to this developing story, I will make everything as simple as possible. Now let’s see how we got here, what this all means and what happens next.

What are UST and LUNA and how the Terra ecosystem works

Terra is a blockchain protocol that is focused around a fiat-pegged algorithmic stablecoin called UST. Terra also has its own token called LUNA that it uses to stabilize the price of UST by control its supply so that 1 UST = 1 US Dollar. This is what people mean when they talk about UST keeping the peg. More on how this mechanism works a bit later.

Terra was founded in 2018 by Daniel Shin and Do Kwon as a Cosmos SDK-built payment/savings-oriented system with the overall ambition to combine fiat currencies and cryptocurrencies into a unique product that people could use without even knowing that they are using blockchain technology. Products like the CHAI wallet aimed to do just this. However, with what at the time of writing seems to be a complete depeg event of UST from the Dollar and the subsequent 97%+ crash of LUNA’s price, these projects are all but gone.

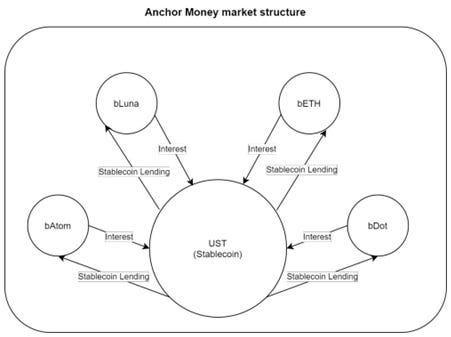

UST is (was) the third largest stablecoin and the most popular algorithmic stablecoin. Its main utility was a (theoretical) money market protocol called Anchor. Right before the depegging event, roughly 40% of all UST was in Anchor. If you think that’s impressive, I’ll have you know that there where times when it was 70%. The incentive to deposit into Anchor was massive: 20% APY on a stablecoin. Terra Labs have recently made changes to that reward system, as a new dynamic yield system was set in place that moved the APY down over time. It reached 18% in May and was supposed to go down to 16% in June.

Who wouldn’t want an easy 20% savings account in a world with almost double-digit inflation and banks that offer you fractions of a percentage?

Anchor protocol paid the 20% to those who deposited their UST through two major funding pipelines: Income + the yield reserve.

· Income: Anchor has several sources of income. These are most notably the deposited UST, and the collateral from bETH and bLUNA, deposited into the platform to be borrowed against. The interest rate is also algorithmically determined through supply and demand. Other smaller sources of income include the 1% liquidation fee.

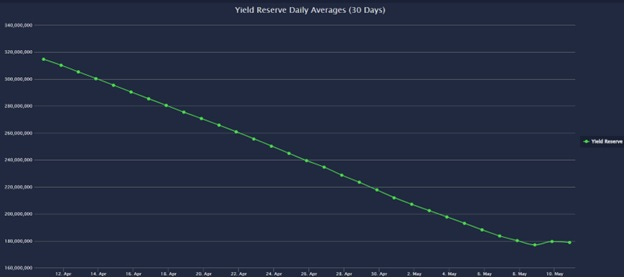

· Yield reserve: The yield reserve is the amount of capital held on Terra in order to sustain the 20% APY. This is where the $1B+ BTC fund that was used to try and regain the peg came from. The yield reserve has been steadily dropping and for the past weeks, Anchor has been losing roughly $5 million a day.

All things considered, after doing the simplest of P&L reports, Terra would have been a sustainable and profitable project with a yield of around 5%. So why did it keep the 20% APY? Very simple: Marketing. Terra effectively paid people to use their platform, with a plan to slowly decrease the APY over time and get more and more users. It might be wrong or disingenuous even, however it is not, under any way shape or form any different to the hypergrowth start-ups of this age, where buying market share and users trumps profits. We live in weird times.

The Terra ecosystem wasn’t just about Anchor though. Projects like Mirror Protocol were also widely used. Mirror used synthetic stocks to make it easy for people who had UST to trade the stock market without going through brokers.

Crash course into algorithmic stablecoins

Now that we have a simplified gist of how the Terra ecosystem worked, how exactly did UST keep its peg day-to-day and how was the system supposed to function long-term? High reserve-backed APYs are all fun for a while, however an algorithmic stablecoin is intended to do just what its name suggests: Algorithmically stabilize the value of one asset to another.

Simply put, a stablecoin is a token whose value is pegged to another asset, typically the US Dollar. Some stablecoins like USDC and TUSD are backed by an equivalent treasury. This means that for every 1USDC that equals 1 USD, there exists 1 real USD in the treasury of those that provide the stablecoin. There are currently roughly $175 billion worth of stablecoins, $146 billion of which are fiat-backed.

Algorithmic stablecoins on the other hand, do not have any collateral backing and have their supply changed in order to reflect the change in market price via different methods. There are currently $29 billion worth of algorithmic and crypto-backed stablecoins in circulation, with UST being the biggest (still as of this writing).

Other algorithmic stablecoins in whole or in part, exist and function with varying degrees of success. MakerDAO’s DAI for example, uses a part-collateralized, part-algorithmic way to hold its peg. What is interesting about DAI is that it’s essentially run by a DAO and is arguably the most stable of stablecoins, being battle-tested again and again.

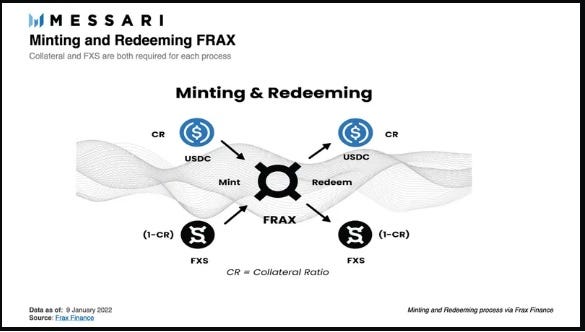

Frax is another example, with a fractionalized collateral method to hold the FRAX peg via two tokens (USDC and FXS) and deep liquidity pools, like for example the FRAX3CRV pool on Curve. If you are interested in how Frax works, Messari did a pretty cool job explaining it here.

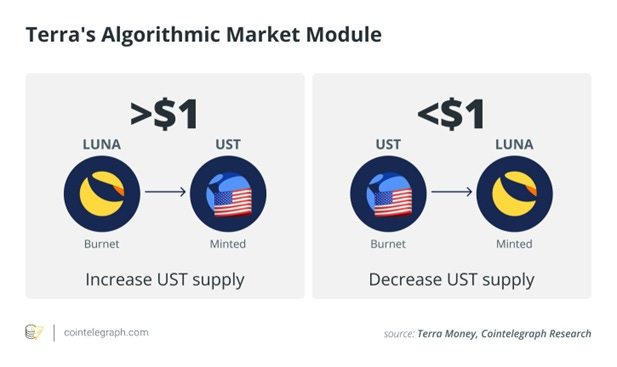

The way the algorithm worked for Terra is as follows: LUNA is essentially responsible to increase/decrease the supply of UST through a burn/mint process, and vice versa. When 1 UST>1 US Dollar, LUNA is burned and UST is minted so that the UST supply increases. Increased supply = less value per UST. Conversely, if 1 UST = $0.99 US Dollar for example, then LUNA is minted in order to burn UST and decrease its supply, thus decreasing its price respective to the US Dollar. Every UST in circulation decreases the circulation of LUNA. Let’s say 1 LUNA = $100. Somebody can then mint 100 UST by burning 1 LUNA. If the LUNA price falls to $1 then somebody can redeem their UST for 100 LUNA.

The UST peg and the Terra ecosystem were kept together by this algorithm + the LFG treasury which took LUNA, and sold it in order to fill up the Anchor yield reserve to pay holders their juicy 20%. The long term strategy and bet that Do Kwon and Terra made was that eventually, once the Terra ecosystem has gained even more users, the relationship between the yield reserve, APY, deposits and collateral would be somewhat sustainable. Burn UST for staking -> LUNA price goes up -> Sell LUNA to fund Anchor. Do this for a sufficiently long period of time and eventually UST becomes the standard stablecoin in crypto, thus making LUNA absolutely moon, which will make it exponentially easier to fund the reserve. Oh how the mighty have fallen.

What comes next for Terra?

The strong depegging of UST and the shakeup of Terra has happened in the past. Twice at least actually. Once back in January with the collapse of Degenbox and the whole Daniele Sesta and Wonderland debacle, that made LUNA crash from just over $100 down to $44. A depegging event also happened in May and the algorithm worked as intended. However, Anchor’s deposit back then was roughly $260 million. It was over $14 billion right before the bank run has happened, dropping it to $3.6 billion.

This isn’t the first time that a stablecoin has collapsed or that a good old fashioned bank run happened in crypto. Iron Finance was a similarly brutal, albeit less costly collapse. So, where do we stand now?

Efforts will be (announced) to be made in order to “fix” the situation, regain the peg, bring back the APY and make the Terra community stronger than ever. I have been in crypto for way too long to be soothed by this type of message.

Although tensions are high now and the Terra subreddit unsettles me with how many suicide posts people are posting, this is not the first nor the last catastrophy in crypto. Terra and UST might have failed but algorithmic stablecoins aren’t going anywhere. Nor shouldn’t they. Eventually, a somewhat stable mechanism will be developed and this can revolutionize not just crypto, but one of the most boring topics in the world: monetary finance.

I will not be speculating too much, since it is still a developing situation and I will definitely be updating this article with the final (?) outcome once the dust has settled. I will also not be guessing left and right on who was the source of the coordinated sell of UST since it’s way too early to know for sure.

I see the same number of people who have put their life savings in a project based on a beautiful promise that was essentially backed by a much too ambitious and greedy model. The calm after the storm will inevitably come and algorithmic stablecoins will still be a part of crypto. Many have lost money and few have made a killing. Time is a flat circle.